- Interest rates have never been lower and stock prices have never been higher. We call those bubbles.

- There are 15 explanations for the stock market bubble, but just one cause of the bond market bubble.

- There are 10 possible bubble bursters, including COVID. Increases in interest rates are among the more likely.

- When (not if) the bubbles burst, baby boomers will suffer dearly.

Throughout history, bubbles are a function of extraordinary popular delusions and the madness of crowds. Lance Roberts

78 million baby boomers are currently passing through the “Risk Zone” that could ruin their retirements. Imagine 78 million people irreparably and simultaneously harmed. Losses sustained during the 5 -10 years before and after retirement will diminish retiree lifestyles even if markets subsequently recover.

This is a terrible time to be retired because interest rates have never been lower, stock prices have never been higher, and the world is in the throes of a debt crisis that could destroy paper (“fiat”) money. Compounding the risk, the average baby boomer is invested 60/40 stock/bonds, a mix that lost more than 35% in 2008, and could lose much more when stock and bond market bubbles burst.

In this article, we show that bubbles currently exist in stock and bond markets and explain why they exist. Then we provide a list of “pins” that could burst these bubbles. It’s not a matter of “if”; it’s how and when. Then we conclude with recommendations for baby boomers that could protect them from these bursting bubbles. Younger people will probably recover, but baby boomers do not have the luxury of time to recover.

Bubbles Are Real, Really

Investors are being Gaslighted into thinking that bubbles do not exist because Wall Street wants them to stay in the markets, but respected experts see otherwise. Here are a few examples that you should watch:

- Ron Surz https://youtu.be/n9QDdtD5wyc

- Jeremy Grantham: https://www.youtube.com/watch?v=RYfmRTyl56w&feature=youtu.be

- Harry Dent https://www.youtube.com/watch?v=lg51JrFpLzk

Bubbles occur when prices become exceedingly expensive. There are several standards that are currently higher than they have ever been, like price/earnings ratios and Warren Buffet’s ratio of stock market value to GDP. The following picture is an example that uses a family of expensiveness measures, from Advisor Perspectives

Stocks are expensive, so it’s reasonable to assume that investors will simply stop buying at some level of overpricing, and the first sellers will be glad they did – no more “buy the dip”. There are several “pins” discussed below that could burst the bubble. The important issue for investors is the loss that could occur. In the following matrix, we show that a 50% loss would occur if Price/Earnings ratios return to their long-term average of 15, but if stocks remain pricey at their current 30 P/E, returns will remain positive.

Source: Target Date Solutions

Bubbles usually don’t last long. You can be the judge of how quickly some pin will burst the current bubble. In February 2020 it appeared that the COVID pandemic would be the pin, but “buy the dip” won that round. The pandemic might still be a contributor; time will tell.

The other bubble is in the bond market. Our government, as well as other governments, are implementing a “Zero Interests Rate Policy” (ZIRP), manipulating interest rates to artificially low levels in order to keep borrowing costs under control on our mounting debt. We have a debt crisis. As discussed below, this crisis is one of the pins that could burst the stock market bubble. The bond market bubble exists because our government wants it to exist. The reasons for the stock market bubble are more complex and varied.

Why the stock market is in a bubble

We can think of 15 reasons for the current stock market bubble, most of which are wishful thinking.

- Investors believe that vaccines will cure the pandemic quickly, and

- Earnings will soar in an economic recovery like no other

- The Federal Reserve will support stock and bond markets, dumping $trillions

- Interest rates will remain low, justifying high stock prices.

- Investor greed: FOMO is fear of missing out

- Investor euphoria: Hopium is the drug that gives hope for a bright future

- Huge foreign demand for US securities. Foreigners fear devaluation of their currencies and view the US as “the cleanest dirty shirt in the laundry basket.”

- 92 million Millennials believe markets only go up and are actively trading on Robin Hood, Robos and the like

- The FAANG Stock phenomenon where investors believe mega-companies will perform well regardless of the economy.

- Apple is worth $trillion and Tesla is worth more than its competitors combined

- The election. The stock market is up so far since Joe Biden took office

- A belief that amateurs can beat Wall Street with short squeezes on the likes of GameStop and silver.

- Stock buybacks capitalize on low borrowing costs.

- SPACs: Special Purpose Acquisition Companies

- IPOs: Initial Public Offerings

Bursting Bubbles

The laws of physics limit the size of bubbles – they all burst when overinflated. They can burst on their own, but most of the time some event triggers a burst, after which everyone agrees that there was a bubble. Two of our most-watched videos are Ten Threats Facing Investors and The Stock Market Will Reconnect With the Economy where we discuss the following threats to the economy and stock market.

Any one of these threats could burst the bubbles, but we think the following scenario is likely:

- Interest rates will rise because:

- A foreign country flinches and raises its interest rates, and/or

- Money printing continues to run amuck and causes rampant inflation, maybe even hyperinflation

- Stock prices will fall because earnings will be discounted at a higher rate

- The government will be forced to monetize the debt in order to pay interest, creating a debt spiral

Money Printing Gone Amuck

Led by Japan, the world is running a money printing experiment that will not end well. Japan earned its reputation as an economy adrift in the 1990s when a popped financial bubble was followed by slow growth, deflation, and low-interest rates. As the government struggled to pry the economy from its rut, it pioneered policies like quantitative easing that were used around the world after the global financial crisis of 2008. Japan has led the way in implementing Modern Monetary Theory (MMT) which some, including me, believe to be the cause of a Global Debt Crisis.

MMT advises governments to print money if they own the printing press, but to guard against inflation by raising taxes as needed. Will politicians have the political will to raise taxes? What do you think? Proponents of MMT say that politicians are the culprit because of their profligate spending, which makes sense. MMT is the “Permission Slip” that authorizes the spending. It’s the “gun” that politicians are shooting at the economy.

Advocates of MMT and money printing point to Japan because their economy has limped along without a serious blow-up, yet. It’s like the optimist falling from a skyscraper saying, “So far, so good.”

As shown in the following graph, Japan’s debt-to-GDP ratio of 400% is leading the world, so the belief is that the rest of the world has capacity. No one knows how much debt will break the bank, but most expect catastrophe when the limit is broken. Japan is poking the bear.

But as shown in the following picture, the US has outdone Japan in providing COVID relief.

As a result, the US money supply has increased by 27%, as shown in the next picture

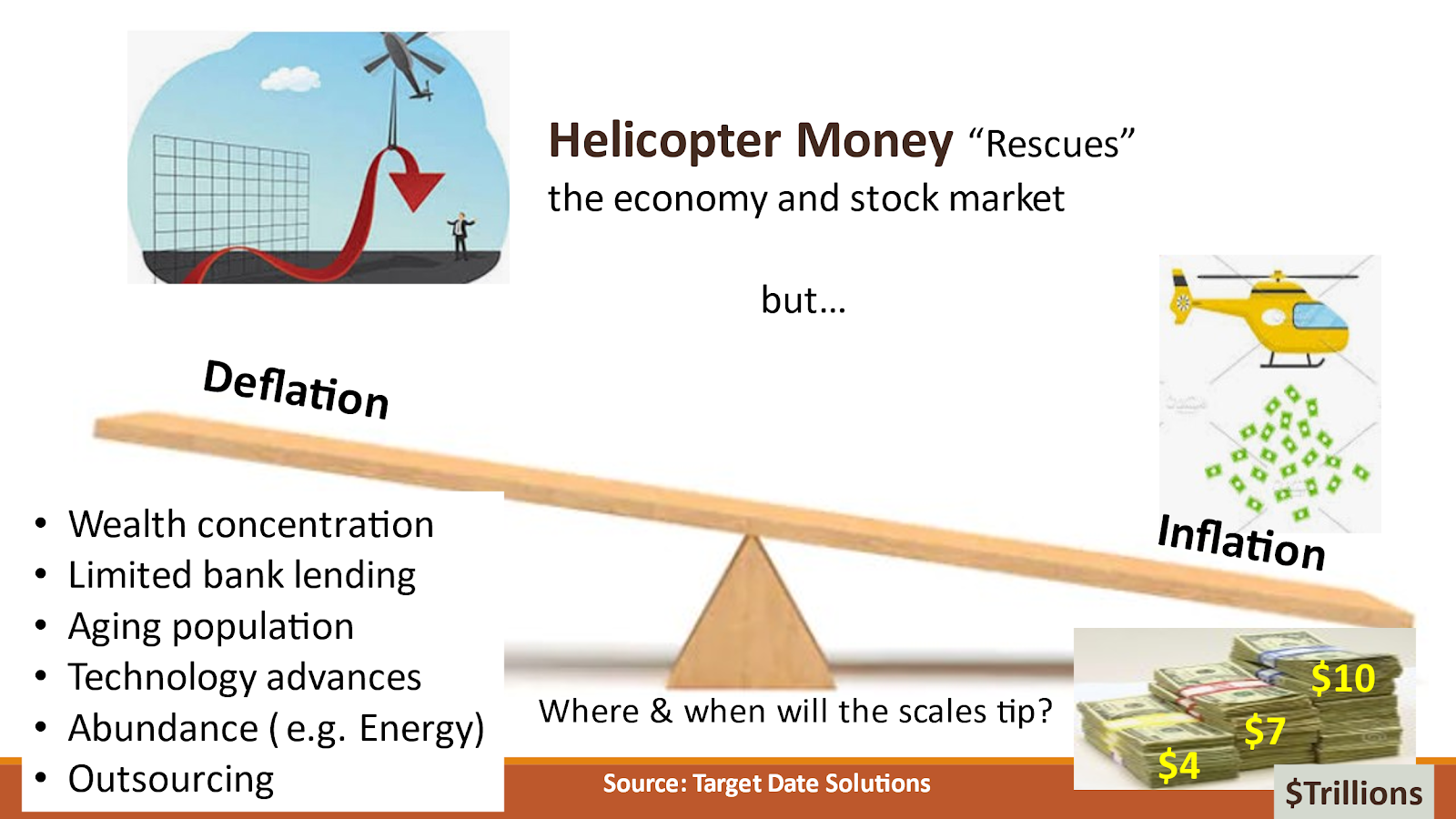

Quantitative Easing (QE) of $4 trillion did not move the CPI needle because that money went into stock and bond markets, creating asset price inflation, but $ 5 trillion in COVID money is being dropped by helicopter into the homes of people who will use it to pay bills and buy groceries, plus President Biden wants to spend another $3 trillion on the Green New Deal. In other words, current deflationary forces will be overwhelmed by mounds of paper:

Paper money is called “fiat currency” because it works by fiat – the government says it works. But the fact is it’s just pieces of paper that only work as long as we all agree and trust. The definition of money is that it is a store of value and a means of exchange. When currencies are devalued by excessive printing, they cease being a store of value. And in the case of extreme devaluation called hyperinflation, billionaires become penniless and paper money can’t be exchanged for anything.

Baby Boomers Could be Ruined

No one knows how much money the US can print without creating inflation, and no one wants to find out, but that is the path we are on. It’s a path that will be extremely painful and devastating to our baby boomers.

Two of my most read articles are Baby Boomers Should Not 'Stay The Course' Because Most Are On The Wrong Course and The stock Market Will Reconnect With the Economy. Baby boomers started transitioning through the Risk Zone in 2006 and will continue until 2034. That’s 3 decades to hope that disaster can be avoided, an unrealistic hope. Some boomers will not make it through the Risk Zone unscathed, but they can protect themselves now before it’s too late.

The number one investment objective of baby boomers at this stage in their lives should be to protect their lifetime savings. The first level of protection is to not invest in overpriced and risky stocks and bonds. The average boomer is 60/40 stocks/bonds, a mix that lost 25% in 2008 and that could lose much more when the current bubbles burst. Ordinarily, cash would be a safe haven, but there is a risk of rampant inflation that argues for protection in precious metals and other real assets like cryptocurrencies and commodities.

Conclusion

Most stock market forecasters choose to ignore the threats that are facing the US economy and stock market, but investors should not allow themselves to be Gaslighted. Younger investors will probably come through the next crash unscathed, but baby boomers cannot be that cavalier because they could find themselves “living under the bridge eating cat food.”

Please see How to Minimize the Impact of Inflation, Recessions, and Stock Market Crashes for some thoughts on protecting yourself. Also, Peak Prosperity is a good source of economic analysis that says it like it is, as does the Baby Boomer Investing Show.

Please take our course on The Bubble Burster here:

https://learnformula.com/course/inflation-brings-crashes-the-bubble-burster

Never miss a post.

We'll keep you in the loop with everything good going on in the modern professional development world.