- Global debt is officially $184 trillion, which is 225% of global GDP. This is $86,000 for every person in the world, which is 2.5 times annual income.

- We estimate that official figures are understated by a factor of 2.5, so debt is actually $460 trillion, which is 560% of GDP and $215,000 per person.

- These numbers are astronomical, raising the risk of economic blowback once interest rates and inflation rise, as they eventually will.

Official World Debt

The International Monetary Fund reports that global debt has reached a record high, raising serious implications for the global economic outlook. The worrisome details include:

- Global debt has reached an all-time high of $184 trillion in nominal terms, the equivalent of 225 percent of GDP in 2017. On average, the world’s debt now exceeds $86,000 in per capita terms, which is more than 2½ times the average income per capita.

- The most indebted economies in the world are also the richer ones. The top three borrowers in the world—the United States, China, and Japan—account for more than half of global debt, exceeding their share of global output.

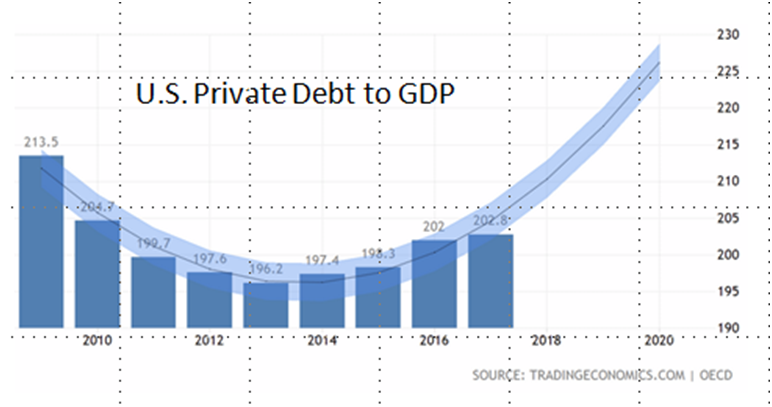

- The private sector’s debt has tripled since 1950. This makes it the driving force behind global debt. Another change since the global financial crisis has been the rise in private debt in emerging markets, led by China. At the other end of the spectrum, private debt has remained very low in low-income developing countries. See the section below on “Why Worry.”

- Global public debt, on the other hand, has experienced a reversal of sorts. After a steady decline up to the mid-1970s, public debt has gone up since, with advanced economies at the helm and, of late, followed by emerging and low-income developing countries.

The Visual Capitalist breaks global debt out by country as follows:

The “Real” numbers are much bigger

The official numbers are understated. In this article, I show that the official US figure of $20 trillion in public debt is 5.5 times less than the actual debt of $110 trillion, which is 390% of GDP. Public debt in the US is about one-third of total debt, so real total debt is 2.5 (5.5 X 1/3 +2/3) times higher than the official number

Using this 2.5 times multiplier applied against the official $184 trillion, global debt is really more like $460 trillion which is 560% of Global GDP. It’s beyond belief.

Why Worry?

Debt brought the world to its knees in 2008. Paradoxically, disaster was circumvented by doubling down with even more debt, deferring the consequences to sometime in the future. That future is rapidly approaching. In The Coming Global Financial Crisis: Debt Exhaustion, Charles Hugh Smith observes:

The global economy is way past the point of maximum debt saturation, and so the next stop is debt exhaustion: a sharp increase in defaults, a rapid decline in demand for more debt, a collapse in asset bubbles that depend on debt and a resulting drop in economic activity, a.k.a. a deep and profound recession that cannot be "fixed" by lowering interest rates or juicing the creation of more debt.

Even if it’s not the cause, debt has a history of predicting market crashes. In A Brief History of Doom: Two Hundred Years of Financial Crises author Richard Vague demonstrates that the over-accumulation of private debt does a better job than any other variable of explaining and predicting financial crises. The 2008 crash is a recent example.

A number of other economists agree. Steve Keen, an economics professor who heads the School of Economics, Politics, and History at Kingston University, outlines a persuasive case in his book “Can We Avoid Another Financial Crisis?” for why rising private debt tops the list of possible triggers for the next financial crisis and recession.

Consider private debt with the current gargantuan public debt and it’s clear that we need to worry about a double whammy of a market crash exacerbated by stagflation, or even hyperinflation. The next recession will also be compounded by the toppling of the share buyback dominoes.

Much of the “real” debt is for government promises that cannot be kept -- Medicare in the US, for instance. These are promises that the people have made to themselves, so it’s conceivable that some generations will simply refuse to pay, causing social disorder.

Foreign affairs may bring trouble, too. The so-called Thucydides’ Trap is a related threat that sees the US and China heading toward war, and everyone’s hoping that it might be a relatively benign conflict like the Cold War that was waged with Russia, or that it might end with a battle using only tariffs as weapons. Yet the great Greek historian Thucydides foretold that irresistible rising forces (like China) would collide with immovable superpowers (like America). Nouriel Roubini, known for his correct warnings of the 2008 recession, believes that the China-US trade war will push the US economy into recession in 2020 or sooner. It doesn’t help that China is one of America’s largest lenders. There’s a good chance that China’s US loans will be withdrawn, or no future loans will be made, leaving the US with limited funding sources. The next time the Debt Limit is raised, Congress might discover that there are no lenders.

Some say that the world has bigger problems to worry about like the possible use of nuclear weapons, and that’s true. No one knows which threat(s) will send the world into turmoil or when it will happen, but we do know that if something cannot go on forever, it will end. All we can do is prepare as best we can.

These Bills Will Not be Paid

The official estimate is that every person on the planet owes $86,000 but we estimate that the actual number is around 2.5 times that amount -- $215,000 per person, which is more than 6 times the average income per capita. In other words, every person on the planet owes 6 years of labor. No one cares at the moment, partly because no one intends to pay their share, but mostly because we choose to deny the problem’s very existence.

The world economy is running on the fumes of delusory borrowed money, playing an outlandish game that will not end well. We owe each other money that won’t be paid in today’s dollars. That’s why cryptocurrencies were invented. Fiat money only works if we all agree to honor it; otherwise, it’s just pieces of paper. US currencies were debased in 1971 when they were taken off of the gold standard and replaced by “In God We Trust.” Now debasing means printing money, or monetizing the debt. Lenders lose when borrowers control payment values.

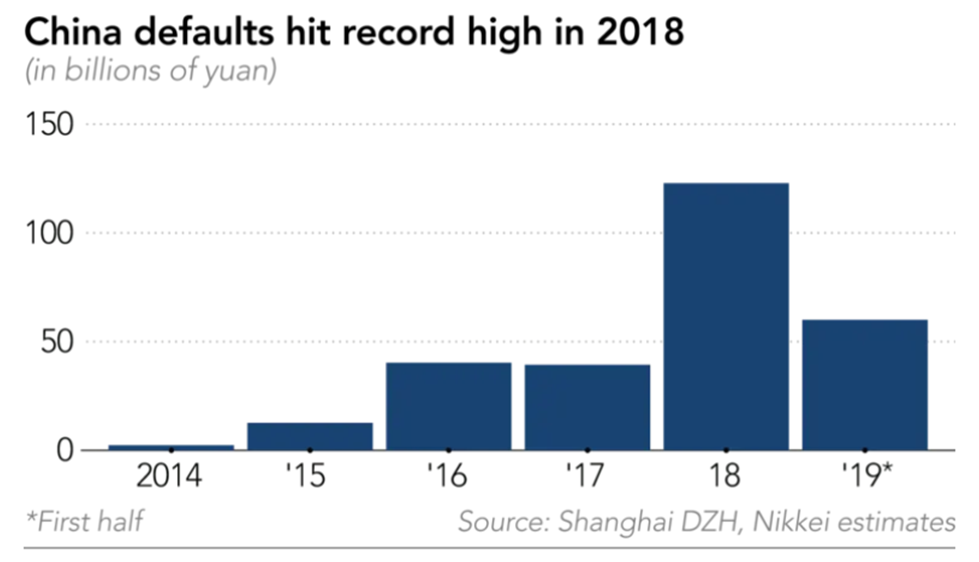

Signs of weakening credit quality are also appearing in China, where 2018 was a record year in corporate bond defaults, and 2019 looks like it will be even worse.

Concerned savers can trust a yellow mineral (gold), lines of code (cryptocurrencies), or baskets of non-US currencies. Economist James Rickards estimates that if gold became the world currency standard its price would rise 700% to $10,000 per ounce from the current $1400 per ounce. If gold is your preference, you might want to invest in the countries that produce the most of it, namely China and Australia.

Despite the current predicament, Modern Monetary Theory (MMT) advocates unlimited government borrowing. Governments “solve” the debt problem by borrowing more.

Modern Monetary Theory

Central banks around the world are fighting the debt fire with gasoline. In the $22 Trillion Question, Institutional Investor magazine questions the validity of MMT that advocates unlimited borrowing, describing this theory as “refuting the laws of macroeconomic gravity.” The late actor and Senator Fred Thompson humorously explain the folly of MMT in this video.

But Research Affiliate Chris Brightman says heterodoxical MMT is here to stay (until it breaks), “partly because it promises to help reverse wealth inequality, which conventional monetary policy has partly fueled.” Also, Nathan Locke of Economic Justice argues that MMT is just fine – the problem is how it’s used; government debt is just a meaningless ledger entry with offsetting financial assets on the other side of the ledger. Debt purchases assets so it’s a wash. “Debt” in this context is borrowed money as opposed to the value of promises like Medicare and Social Security.

But something is awry when in June of 2019 government debt around the world was priced at negative yields and central banks were signaling more easing. How crazy is that? Investing is the idea that you delay consumption now for consumption later in the expectation that your future consumption will be higher. This guarantees delayed consumption now for lower consumption later. As a consequence, gold prices broke through $1400 per ounce and many saw it heading toward a historic $1800 high. It would appear that investors are scared, as they should be.

Altogether, a jaw-dropping $13 trillion in global government debt—a new record—was offering sub-zero yields in June 2019. Investors are guaranteed to end up with less than the bond’s principal amount if held until maturity. There are no “safe investments,” so it’s a dreadful time for everyone who’d like to protect their savings; investments with guaranteed losses are not safe.

Negative yields have driven investors to gold as a safe harbor and as providing the prospect of at least maintaining value. Central banks are also loading up on gold, recognizing that the imminent liquidity trap will render further actions ineffective; the game is ending.

The world is on track to suffer debt exhaustion since there is presumably some limit to how much borrowing the world economy will accommodate. No one knows when the debt spiral will end, but it’s a virtual certainty that it will not end well.

Now might not be the most opportune time to abandon the U.S. stock market. Martin Armstrong, the economic forecaster, sees the U.S. stock market as “the cleanest dirty shirt” in a world laundry basket headed for ruin. In July 2019 Armstrong predicted: With so much of the rest of the world beginning to succumb to the arriving global recession, capital is fleeing towards the relative safety and positive returns offered by America’s financial markets. As a result, I see the US stock market continuing to power higher from here, with the Dow Jones Industrial Average potentially tagging 35,000 by 2021.

You can hang in there for the last gasping breath in the U.S. stock market or you can move to protect now. Hanging in for a lifetime is a high-risk gamble for young people, but the biggest immediate pain will be felt by the world’s hundreds of millions of Baby Boomers, many of whom will become dependent on societies that can’t afford to help. Old folks have the most to lose because they won’t be able to recover. According to Edward Siedle, 401(k) expert, Too frail to work, too poor to retire will become the “new normal” for many elderly Americans.

How to Protect Yourself

“You cannot fix a problem that you refuse to acknowledge.”

― Margaret Heffernan, Willful Blindness: Why We Ignore the Obvious at Our Peril

Sticking our collective heads in the sand and hoping the problem goes away is not a solution. But no politician who wants to stay in office will acknowledge the problem and deal with it. They want to delay the day of reckoning, but this delay cannot be indefinite. We need to protect ourselves because our leaders will not.

Treasury bonds will not provide the safety that they have historically offered because they’re at the heart of the problem: financing the debt. A well-diversified portfolio of inflation-protected assets will help, like Treasury Inflation-Protected Securities (TIPS), commodities, and real estate.

There will always be life events to which we each react in our own ways. Since we only get one life path, each decision is very important. Today’s decisions weigh heavily on our future, so it’s important to have a lifetime investment plan that puts today’s decisions into perspective.

Please take our course on the Debt Crisis here https://learnformula.com/course/the-debt-crisis-with-professor-laurence-kotlikoff

Ron Surz wrote the book Baby Boomer investing in the Perilous Decade of the 2020s

Never miss a post.

We'll keep you in the loop with everything good going on in the modern professional development world.