- Social Security benefits can accumulate above $1 million

- Medicare is subsidized, reduced cost, health insurance

- Medicaid is help for the needy

In the previous chapter on Living to 100, we report that most baby boomers rely on Social Security and Medicare to provide a reasonable standard of living, and we also report the costs to taxpayers of these awfully expensive programs that are forecasted to go bankrupt soon. In this article, we discuss the choices that beneficiaries make and how to avoid mistakes.

Social Security

Background

The Social Security Act was signed into law by President Roosevelt on August 14, 1935. In addition to several provisions for the general welfare, the new Act created a social insurance program designed to pay retired workers age 65 or older a continuing income after retirement. The first one-time, lump-sum payments were made in January 1937. Regular ongoing monthly benefits started in January 1940. Cost of Living Adjustments (COLAs) was first paid in 1975 as a result of a 1972 law. Prior to this, benefits were increased irregularly by special acts of Congress.

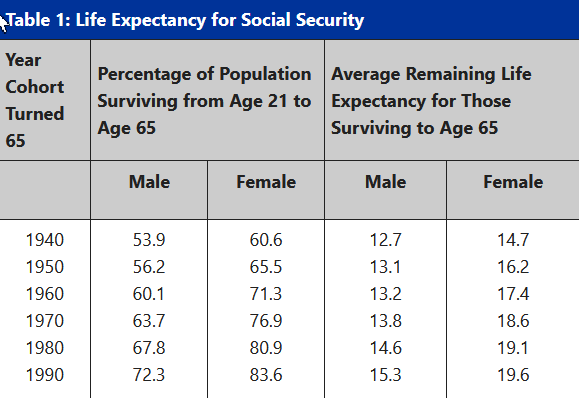

As reported in the previous chapter, Social Security has become increasingly expensive because people are living longer, as reported by the Social Security Administration:

Cost

Taxes were collected for the first time in January 1937. Social Security payroll taxes are collected under the authority of the Federal Insurance Contributions Act (FICA). The payroll taxes are sometimes even called "FICA taxes." FICA is nothing more than the tax provisions of the Social Security Act, as they appear in the Internal Revenue Code. For 2021, the FICA tax rate for both employers and employees is 7.65% (6.2% for Social Security and 1.45% for Medicare). For 2021, the Social Security tax rate is 6.2% each for the employer and employee (12.4% total) on the first $142,800 of employee wages. There is no salary limit on the 1.45% Medicare tax. These taxes are paid while you are earning (accruing) benefits.

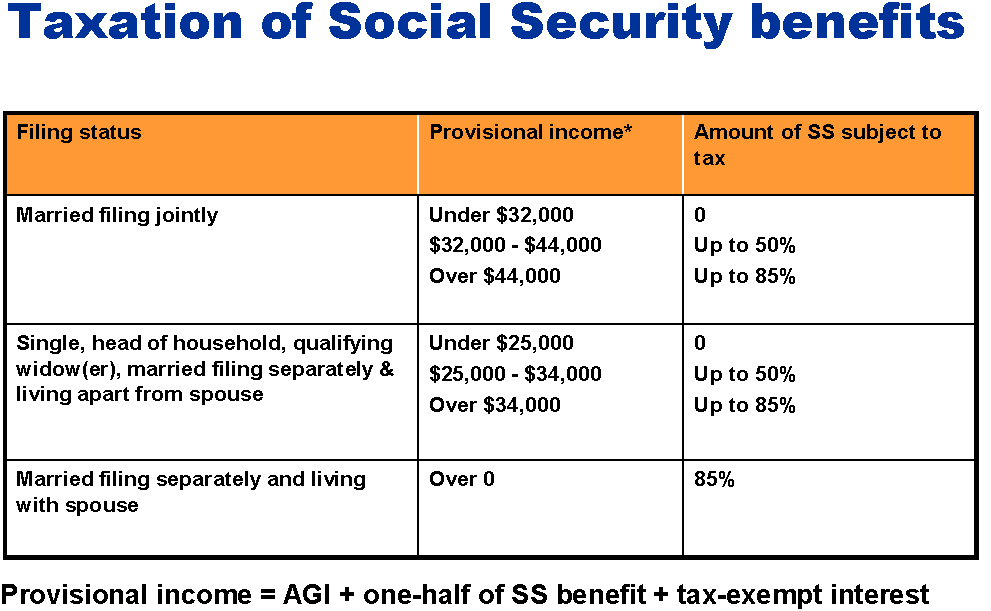

You might also pay taxes on your benefits if you earn an additional income:

As reported in the previous chapter, these taxes are insufficient to pay current benefits, so the shortfall adds to the spending deficit. As people retire, the reliance on those who remain working increases.

Choices

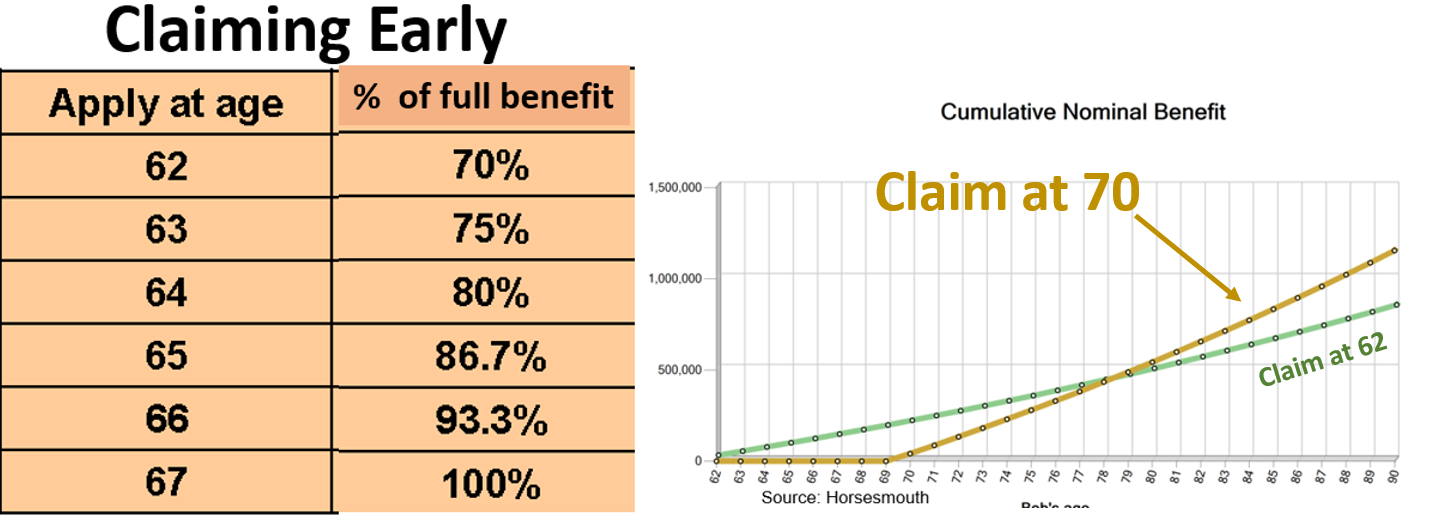

Your main choice is when to claim benefits. This is an important choice that you should research and use available consulting services. You can claim early reduced befits at age 62, full benefits at age 67, or delayed (increased) benefits at age 70. Most Social Security advisors recommend that you wait as long as you can in order to earn the maximum benefit as shown in the following graph

General decision guidelines are as follows:

- Early (age 62) if you really need the money, don’t expect to live long or fear that Social Security will end

- Full (age 67 at this time) if you expect to live a normal length of life

- Late (age 70) if you don’t need the money at age 67 and you expect to live a long life

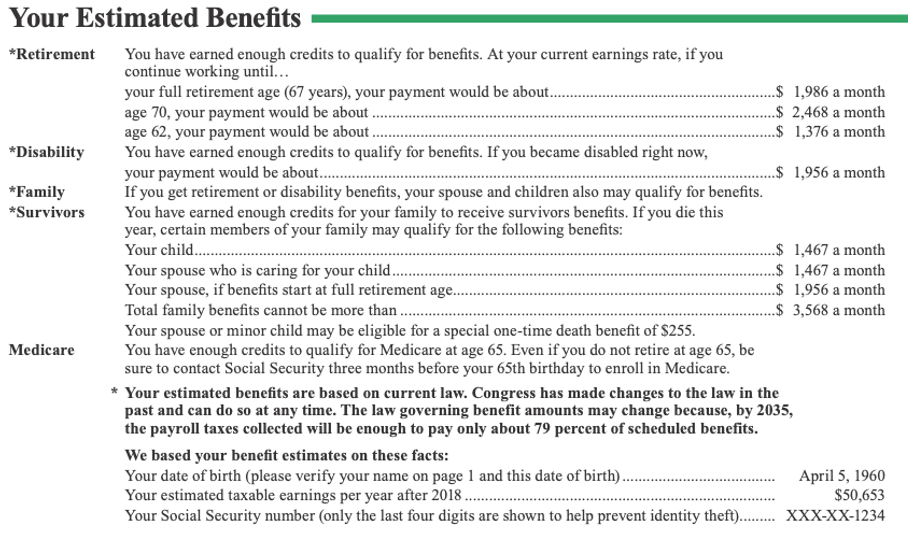

The Social Security Administration provides information to help you make this decision, like the following sample benefit report:

Survivor benefits are an important aspect of your decision that is complicated so you should seek professional guidance. Sometimes you can amend your decisions, but it’s best to get it right the first time.

Medicare/Medicaid

Background

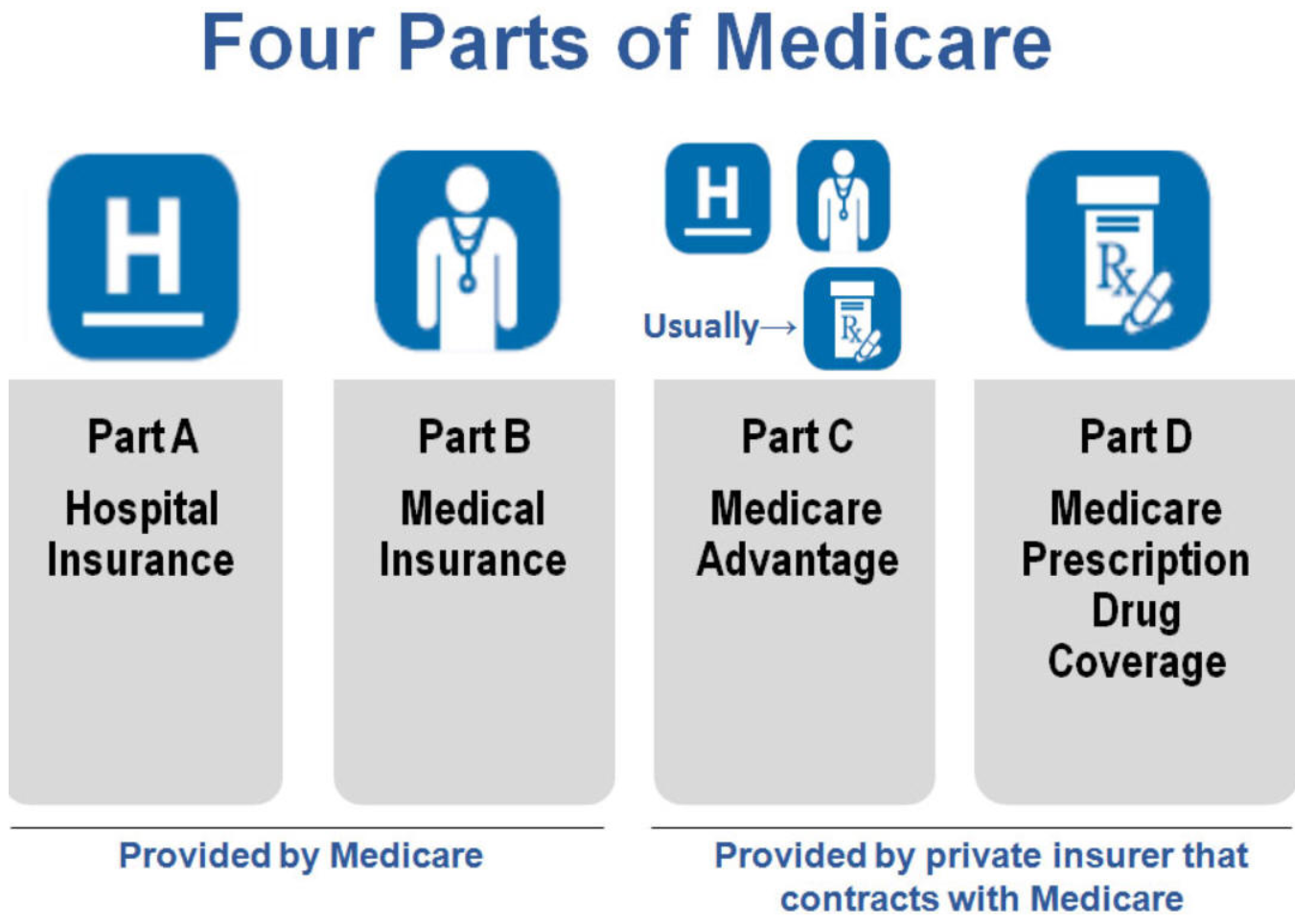

On July 30, 1965, President Lyndon B. Johnson signed into law legislation that established the Medicare and Medicaid programs. There are four parts to Medicare coverage as follows:

Medicaid provides health coverage to millions of Americans, including eligible low-income adults, children, pregnant women, elderly adults, and people with disabilities. Medicaid is administered by states, according to federal requirements. The program is funded jointly by states and the federal government.

Costs

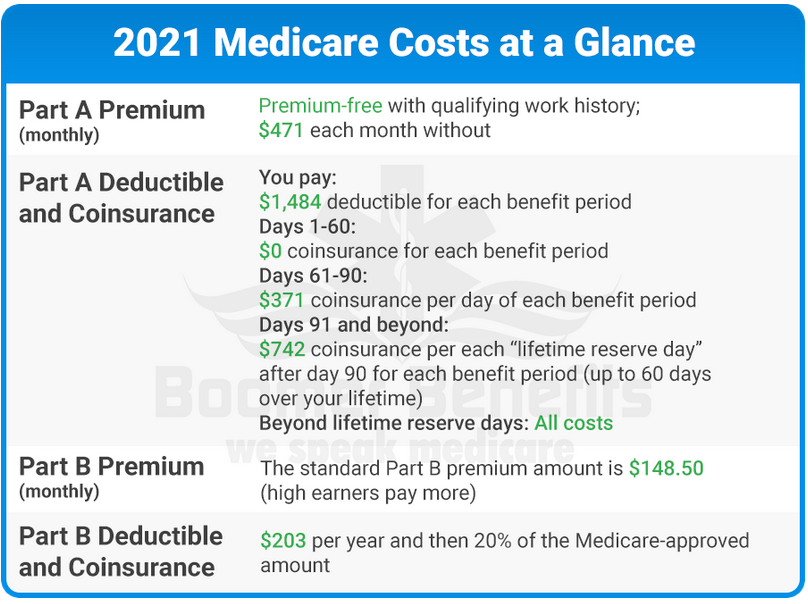

As discussed above, FICA taxes currently at 1.45% pay some Medicare/Medicaid expenses. Most people don't pay a Part A premium because they paid Medicare taxes while working. If you don't get premium-free Part A, you pay up to $471 each month. Most people pay the standard Part B premium amount ($148.50 in 2021). Those with high adjusted gross incomes pay more. Deductibles and co-insurance for Part B are shown in the following table. The costs of parts C and D vary as explained in the next section.

Choices

Medicare Parts A and B provide basic coverage that is insufficient for most people who get sick. There are two basic ways for recipients to fill most of the coverage gaps and reduce the risk of tremendous bills in a bad health year:

- Medicare plus Medigap supplemental insurance policies

- Medicare Advantage Plans

Most recipients purchase additional Medigap insurance that comes with a whole range of coverages and costs. Websites help you search for a plan that matches your needs and budget, but we recommend that you use an insurance specialist. In addition to covering the gaps in “Original Medicare” supplemental plans typically provide dental and eye care benefits. You can also choose a separate provider for Part D prescription coverage, or you can purchase it from your Medigap provider. The choice here is coverage and cost. You’ll want to see what it will cost you for your prescriptions; “formularies” can vary widely across providers.

Many cannot afford Medigap supplemental insurance, so a Medicare Advantage Plan, also called Part C, is a good choice. Many Advantage plans are free or low-cost and include prescriptions. Most Medicare Advantage plans operate as a health maintenance organization (HMO) or preferred provider organization (PPO) insurance. HMOs limit members to using the doctors and hospitals in their networks. PPOs generally let members get care outside the plan's network, but members may have to pay more for such care. Some plans require prior authorization for specialist care or procedures, or a referral from a primary care doctor. Plans might not cover care given outside of the network’s geographical area. Extra benefits not covered by regular Medicare, such as eyeglasses, routine dental care, or gym memberships, may be offered.

Medicaid

Medicaid is discussed in our article on “Living to 100.” It can be extremely helpful to the poor. The main cost is assigning your Social Security benefits to the care facility that accepts you.

Conclusion

Important generous programs have been created for older people. Ultimate benefits are directly tied to decisions made by recipients, so choose wisely and get help.

Please Take These Courses:

Social Security https://learnformula.com/course/social-security-basic-rules-and-strategies

Medicare & Medicaid https://learnformula.com/course/medicare-and-medicaid

Never miss a post.

We'll keep you in the loop with everything good going on in the modern professional development world.