Investment consulting has a long history that has been marked by innovations occurring about every ten years.

In the following, we discuss each innovation, plus the impacts of the Employee Retirement Income Security Act (ERISA) and the groundbreaking study on the Importance of Investment Policy.

It is incredible that the “Modern” Portfolio Theory is about 70 years old. It has stood the tests of time and is currently embraced by many consultants. Dr. Harry Markowitz won a Nobel prize in 1990 for educating investors on the magic of diversification and the existence of an “Efficient Frontier” that maps portfolios that earn the highest expected return for a given level of risk. The following graph forms the basis for MPT (Modern Portfolio Theory):

Every stock and bond has a risk and expected return. Risk is measured as the standard deviation of returns – volatility. Investors will only take risks if the expected return is high enough. The graph shows examples of stock and bond risk-reward. The big breakthrough is that combinations of stocks and bonds earn higher returns for the risk, shown along the Efficient Frontier. Diversification is an immensely powerful investment tool.

12 years later Dr. William F. Sharpe extended the work of Dr. Markowitz by introducing the Capital Asset Pricing Model (CAPM) that postulated that everyone should want to hold the most diversified portfolio because it provides the highest return-to-risk ratio, called the “Sharpe Ratio.” The most diversified portfolio is the “World Market” of all risky assets in the world, held in proportion to their market values. An integral aspect of the theory is the “Capital Market Line” which states that risk is best controlled with cash. Every investor should want to hold the Market Portfolio, and if this is too risky use cash to reduce risk. The resulting line dominates the Efficient Frontier, providing higher expected returns for the risk. This breakthrough is not used much by consultants because they prefer to not control risk with cash. However, most consultants use alpha and beta regression statistics that were first introduced by CAPM.

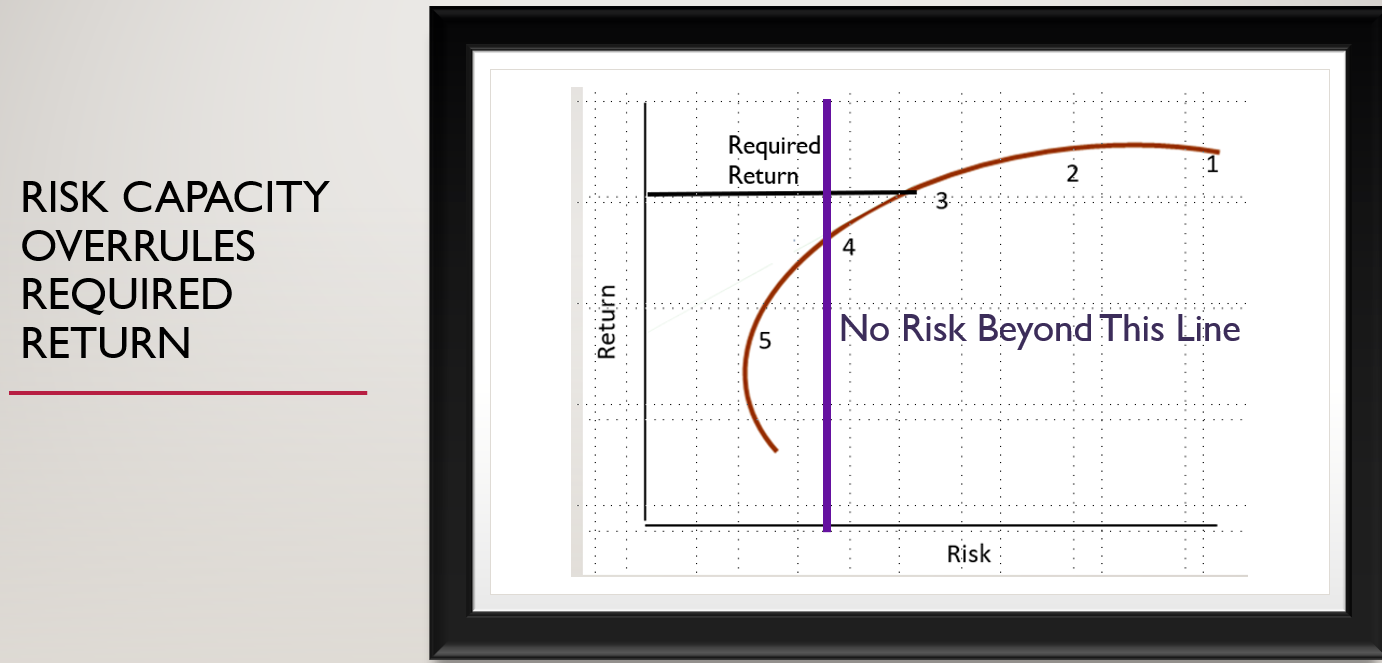

Mapping Risk Tolerance into Models

In the early days of consulting, MPT was used to map a client’s risk tolerance into a model portfolio, as shown in the following graph.

The original idea of “risk tolerance” is the maximum risk that the client can tolerate because high risk earns high returns. This approach changed in the 1990s with the introduction of objective-based investing, discussed below. As shown along the curve above, model portfolios are located on the Efficient Frontier. Then risk questionnaires identify investor risk tolerance that is used to find the best model. The “60/40 Rule” emerged from this practice because most mappings gravitate to the middle toward Model 3 in the graph above. The broad use of the 60/40 rule remains entrenched today. The typical investor is 60/40 equities/bonds, so model providers and TAMPs (turnkey asset management platforms) tend to focus on this model.

1974: The Employee Retirement Income Security Act

About 50 years ago Congress passed ERISA to govern the practices of fiduciaries. This law remains today as the teeth for prosecuting bad fiduciary behavior. Importantly for consultants, parts of the law reinforce the wisdom of diversification to avoid the risk of large losses. Ironically, 12 years later the next innovator showed that you cannot diversify and win the investment performance game. You have to make big bets.

Dr. Robert A. Haugen is the father of factor-based investing. A prolific writer, Dr. Haugen wrote hundreds of articles and books on identifying investment factors that produce alphas, superior returns. These factors include fundamentals like yield and capitalization and classifications like industry sector and style. Dr. Haugen set the academic profession on its ear with the heresy that broad markets can be beaten. His legacy is the fairly common use of factor-based investing today and the recent “discovery” of “Smart Beta.”

Dr. Haugen identified the existence of a return premium in minimum variance portfolios, as shown in the next graph. Today it is called Smart Beta.

1986: The Determinants of Portfolio Performance

In apparent contradiction to Dr. Haugen’s work, a famous study was released in 1986 documenting that asset allocation explained most of the investment performance. The allocations to asset classes like stocks and bonds explained virtually all of the performance in pension funds. A careful read reveals that the report is actually about volatility, as measured by R-squared. Asset allocation explained about 95% of the volatility in portfolio performance. Using the same data provided in the article, we find that asset allocation actually explained 100% of performance.

So how does this square with Haugen’s work? Most pension portfolios were not using factor-based investing in the 1980s, and that fact remains today. Only a few institutional investment firms utilize factor-based techniques.

About 30 years ago, Dr. Frank Sortino, AKA Dr. Downside, proposed a new way to define risk and introduced PMPT – Post Modern Portfolio Theory. Risk in the PMPT world is the possibility that you will not achieve your objectives. Objective-based investing was born, as was the now popular Sortino Ratio.

Dr. Sortino wrote two books on portfolio construction designed to achieve objectives and has made his software available for free, including source code. Consultants use a simplified version that begins by solving for a rate of return that will achieve the client’s objective. Dr. Sortino calls this the Minimum Acceptable Return (MAR). The MAR is then used to locate a model on the Efficient Frontier, as shown in the graph on the right:

Note the similarity between the old risk-based approach and the new objective-based process. Both use a family of models along the Efficient Frontier. Risk-based uses the horizontal scale (risk) to locate a solution, while objective-based uses the vertical scale (return) to find an answer. This reliance on a handful of models was about to change, as discussed in the next section.

The consulting industry had an epiphany about 15 years ago that is slowly being integrated into consulting practices. Risk is more complicated than the volatility or required return. The epiphany is simple, but very important – age matters. There is a time in everyone’s life when we cannot afford to take risks. Losses sustained during the Risk Zone spanning the 5-10 years before and after retirement can ruin retirement, even if markets subsequently recover. Target date funds (TDF) are supposed to provide this protection, although most currently do not. A properly constructed TDF should be no more than 30% in risky assets at the target date, but most are more than 80%.

A TDF follows a “glidepath” that begins with high risk for young investors and reduces risk through time as the target date approaches. The target date in retirement plans is the retirement date. In other situations, the target date is a date that the fund will be liquidated, like the date a student will start school in college savings plans.

TDFs were not very popular before the passage of the Pension Protection Act of 2006, which made TDFs a Qualified Default Investment Alternative (QDIA) in 401(k) plans. Subsequently, TDFs have grown to more than $2.5 trillion. They are the biggest deal in pension plans.

The breakthrough for consultants is that a brake needs to be applied to whatever process is used to find a model. That brake is called “Risk Capacity” defined as the limit on what an investor can afford. Investors in the Risk Zone cannot afford much risk.

The most recent innovation is about investing for retirees. Dr. Wade Pfau and Michael Kitces have conducted extensive research on optimal investing in retirement and conclude that it is best to begin retirement cautiously with no more than 30% in risky equities and bonds and to gradually increase risk through time. The cautious beginning is to protect the Risk Zone, and the re-risking is to extend the life of investments. To begin retirement cautiously you need to end your working life the same way with no more than 30% in risky investments. In other words, a U-shaped lifetime glidepath is optimal, with the bottom of the U in the Risk Zone. Couple this with the importance of asset allocation, and you have the current best thinking for investment consulting.

Dr. Wade Pfau is a professor of retirement income and a Director of the New York Life Center for Retirement Income and Michael Kitces is a consulting industry luminary.

Conclusion

A lot has improved in 70 years, but not all consultants have evolved. Investment consulting is a credence good like computer technicians and car mechanics. “Trusted advisors” are usually nice people, but not all are financially skilled with the clients’ best interests at heart. The client is best advised to trust but verify. Consultants are best advised to differentiate through innovation.

Take Our Course

https://learnformula.com/course/the-70-year-history-of-investment-consulting

References

Brinson, Gary P., Randolph Hood and Gilbert L. Beebower. (Jul-Aug, 1986). Determinants of Portfolio Performance. Financial Analysts Journal. Vol. 42, No. 4 , pp. 39-44

Haugen, Robert A. (1999). The Inefficient Stock Market: What Pays Off and Why. Prentice Hall

Markowitz, Harry (March, 1952). Portfolio Selection. Journal of Finance, Vol. 7, No. 1. pp. 77-91

Pfau, Wade D. and Michael Kitces (12 September 2013). Reducing Retirement Risk with a Rising Equity Glide-Path. Working Paper 2324930 on SSRN

Sharpe, William F. (Sep., 1964). Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. Journal of Finance, Vol. 19, No. 3, pp. 425-442

Sortino, Frank A. (2009). The Sortino Framework for Constructing Portfolios: Focusing on Desired Target Return to Optimize Upside Potential Relative to Downside Risk. Elsevier

Never miss a post.

We'll keep you in the loop with everything good going on in the modern professional development world.