Target date funds (TDFs) are enormously successful, having grown from nothing to $2.5 trillion in just the past decade. Their main appeal is that someone has done all the thinking, so the investor can sit back and relax – their only jobs are depositing and spending money. Most assets in TDFs are from financially unsophisticated participants in 401(k) plans who have defaulted their investment decision to their employer. TDFs are the most popular fiduciary choice of QDIA (Qualified Default Investment Alternative). Defaulted participants do not have the education to think about investment decisions. These TDFs are for people who don’t want to think. Will Rogers said, “Everyone is stupid, but about different things.”

TDFs manage risk through time along what is called a glide path. Young investors take a high amount of risk and old investors take a low amount. The fund provider defines “young” and “old”, and “high” and “low”, but not to worry because it’s the same definition for everybody in a particular TDF. These definitions vary somewhat across providers, but not that much. Uniformity is the consequence of an oligopoly of just 3 firms that manage more than 60% of the $2.5 trillion. It’s been a very profitable product for these fortunate investment companies.

So what do investors give up when they decide not to think, to entrust a TDF to think for them? Control of their destiny. Millions of investors in TDFs are bonded together on a ride to who knows where trusting their employers and hanging on to the hope that there’s safety in numbers.

TDFs for Thinking People are Individualized Portfolios

But no one has to buy a one-size-fits-all off-the-shelf TDF, especially individual investors in Individual Retirement Accounts (IRAs) and those who are managing their 401(k) fund selections. You have your individual needs and circumstances that should drive your investment decisions. You are different from those in a particular fund in the following ways:

- Risk tolerance

- Goals

- Circumstances like wealth, health, and family

We help you create a portfolio that meets your individual needs and circumstances. The process is similar to “building” your dream car with the features and options you like. We walk you through the choices and make recommendations.

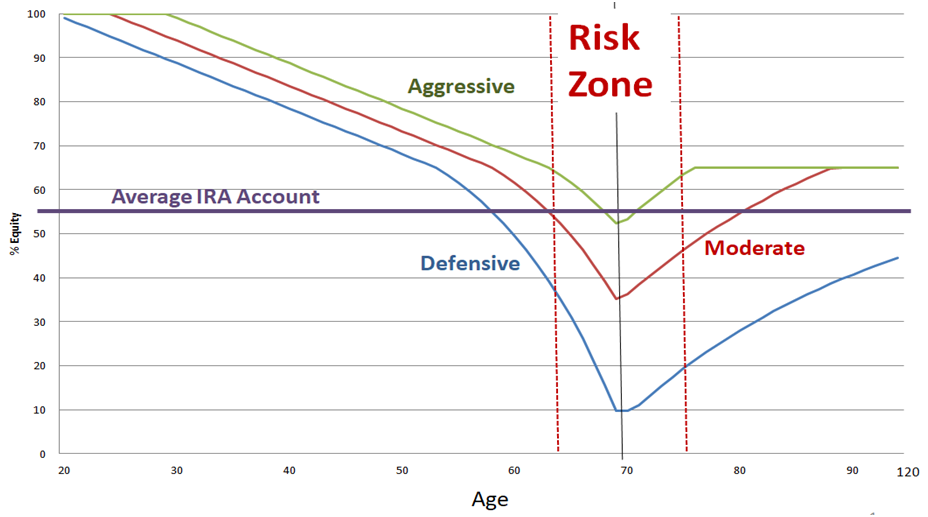

The TDF model is helpful for this guidance as it leads to what we call a Target Date Portfolio (TDP). The key to a comfortable retirement is to (1) save enough, and (2) keep it. TDFs have elements of this discipline that can be improved upon by individual investors who follow a TDP. A wise investor protects his/her lifetime of savings in the Risk Zone that spans the transition from working life to retirement. A generic TDP is shown as the red line in the following picture:

Choosing a TDP Glidepath

A TDP protects assets by reducing risk as savings grow. You can decide how much risk control you want and need. A Conservative glidepath provides the most protection in the Risk Zone, but this protection comes with a possible opportunity cost if markets perform well. We recommend this choice because it maximizes the protection of your lifetime savings, but you can opt for more risk. If you choose an Aggressive glidepath, you’ll follow the path of most mutual TDFs. And then a Moderate risk choice is in the middle between Conservative and Aggressive.

A Couple Fund Choices

We use a family of low-cost mutual funds and Exchange Traded Funds (ETFs) to manage your chosen TDP glidepath, plus we provide two more choices: risk mitigation and socially responsible. If you choose to mitigate the risk in your stock portfolio, losses are limited by about one-half, so for example a 20% stock market loss will reduce your stock holdings by only 10%. The cost for this mitigation is a reduction in upside capture. In essence, we place guardrails around your stock portfolio performance.

The most recent version of socially responsible investing is called “ESG”: Environmental, Social, and Governance. The idea is to have your money work for the common good, but without giving up much in investment return. If you’d like, we can use ESG funds, but be aware that these funds are 2-3 times more expensive than the passive funds we ordinarily employ and no one really knows if they will perform well or poorly relative to our usual passive funds.

Your Personalized Target Date Portfolio

We guide you through these important risk decisions. In the end, you’ll have a custom-built TDP tailored to your needs and circumstances. No cookie-cutter solution for you. Asset allocation is your most important investment decision, and this decision is based on your own personal risk preference. We help you make this important decision using a patented target date framework and we create a well-diversified personal portfolio just for you.

Please take our course on Life Path Investing here https://learnformula.com/course/lifepath-investing-age-matters

Never miss a post.

We'll keep you in the loop with everything good going on in the modern professional development world.