The $trillions invested in Target Date Funds (TDFs) and Individual Retirement Accounts (IRAs) are destined to be devastated by a risk that is well documented but generally unrecognized. Sequence of Return Risk will destroy lifestyles and this time it will be much worse than 2008. Fortunately, each of us can control this risk because it’s personal, but not if we wait until it’s too late. We only get one chance in a lifetime to dodge this risk. Unlike other risks, this risk is individualized and we know when it is greatest so we can protect or take the gamble that losses won’t occur in our own personal Risk Zone. It’s like a sky-diving risk where there is little chance of recovering from being unlucky; the odds of bad luck may be low but the consequences are huge.

All investors knowingly take some risk of losing money, but there comes a time in all of our lives when, unless you do something about it, the risk of loss morphs into the risk of ruin. We all run the mandatory gauntlet of ruin as we transition from our working lives into our retirement years. Losses sustained during this transition period can devastate lifestyles even if markets subsequently recover. That is why Professor Moshe Milevsky calls this the Risk Zone. Most investors are unaware of this risk so it is exceedingly high. It could and should be much lower, as we explain in the following. Unless you feel extraordinarily lucky, you want to be protected against a sequence of return risks. It’s a risk that can and has blindsided many investors. Don’t let this happen to you.

Sequence of Return Risk Defined

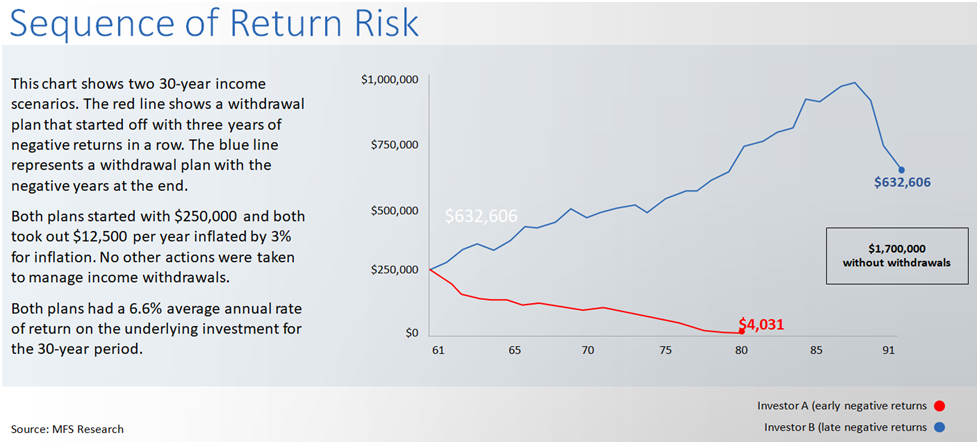

The mathematics of investment return is complex when investment withdrawals come into play. Without withdrawals, the sequence of returns doesn’t matter. We can rearrange return sequences in any way we want and the compound cumulative return is unchanged. Ending wealth is the same regardless of the order in which returns are earned. But if we are withdrawing money, as we are in retirement, the sequence of returns matters a lot. Losses in earlier years can be devastating, while the same losses in later years don’t matter much. Here’s an example:

Managing Sequence of Return Risk

The simplest and most dependable way to manage the sequence of return risk is to keep your investments safe during the Risk Zone that spans the five years before and after retirement. This will of course create opportunity costs if markets perform well, but it is a price well worth paying because you only get to do this once. Your savings are likely to be at their highest as you transition from working life into retirement, so there is more to lose. Behavioral scientists tell us that we feel the pain of loss much more than the benefits of gain. “Save and protect” is a very good mantra for retiring with dignity.

IRAs are exposed to excessive loss in the Risk Zone. The Employee Benefits Research Institute (EBRI) report on IRAs reveals that equity allocations are approximately 55% across all ages, a surprising reality. TDFs are also exposed to excessive risk, with an average 55% allocation near the target date. This is the allocation that lost 30% in 2008, and risk has increased since. To guard against the devastation that lies ahead, IRAs and TDFs should have very low risk in the 5-10 years before and after retirement, but they don’t.

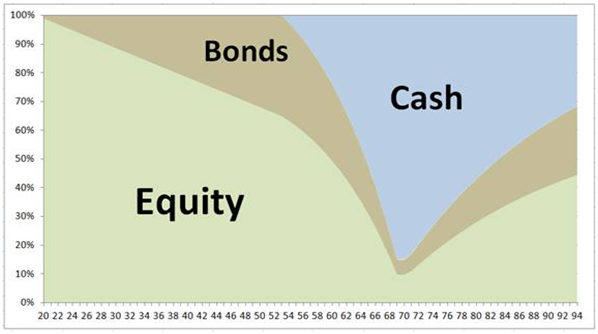

Outside the Risk Zone, a modified TDF glidepath makes sense. Target date funds are more aggressive when you’re young and move to defend as you approach retirement. The problem is that off-the-shelf TDFs are not conservative enough at the target retirement date to defend against a sequence of return risks, so this needs to change. Risk at the target date should be much lower to defend against sequence of return risk, with no more than 10% in equities and the balance should be in very safe assets like Treasury Bills and short-term TIPS. In other words, the “glide path” for defending against a sequence of return risk is similar to TDFs when you’re younger but much safer as you pass through the Risk Zone.

Moving beyond the Risk Zone into retirement most retirees cannot live on T-bills and short-term TIPS, so there needs to be a re-risking in retirement, although no mutual fund TDF does this. What is the “right” glide path beyond the target date? This question is addressed in Dr. Wade Pfau and Michael Kitces’ Reducing Retirement Risk with a Rising Equity Glide Path, where they compare and contrast increasing equity glide paths to flat glide paths in retirement.

K&P conclude: the results reveal that rising glidepaths are even more effective, especially when they start off conservatively. The most favorable (i.e., least adverse) shortfall actually occurs with a glidepath that starts at only 10% in equities and rises to “only” 50% in equities.

In other words, a V-shaped glide path defends against a sequence of return risks and is the best path in retirement for making savings last a lifetime. The bottom of the V is the Risk Zone and should be no more than 10% in equities.

Equity allocations in IRAs should also follow this V-shaped guidance, with no more than 10% in equities for those near retirement.

Diversification

Outside the Risk Zone, it’s wise to take risks in the most diversified way possible, allocating to global stocks and bonds as well as alternatives like real estate and commodities. Diversification is the only free lunch in investing, providing the best returns for the risks taken.

The following glide path incorporates the preceding recommendations.

The Patented Safe Landing Glide Path®

There is only one glide path that manages the sequence of return risk and broadly diversifies outside the Risk Zone. The patented Safe Landing Glide Path® looks like this:

All asset classes are well diversified. Equities are global stocks plus real estate. Bonds are global bonds, and Cash is Treasury bills and short-intermediate TIPS (Treasury Inflation-Protected Securities). See the discussion on cash below.

Our design is patented because it uses financial engineering that no one else has: it’s proprietary and powerful. Importantly, it governs the trade-off between growth and safety, with an emphasis on protecting your savings. See our paper on financial engineering

This glide path provides optimal protection in the Risk Zone, but some investors prefer to be less conservative, so we’ve created the two additional more aggressive glide paths shown in the following.

Note the departures from the average IRA account balance. The average IRA account balance is 55% in equities regardless of age. This is likely a throw-back to the old 60/40 rule that provides good diversification. We’ve learned a lot since the 1980s and TDFs have played a big role in our evolution. Here’s a summary of the differences:

- All glide paths are more aggressive than the average IRAs of young people, prior to the Risk Zone

- The Safe Landing Glide Path is more defensive than the IRAs of people over 60 years old

- The Moderate path is safer for people between 65 and 80, but more aggressive for those older than 80.

- The Aggressive glide path is generally more aggressive than IRAs of all ages

A Word on Cash

Some advisors have reacted negatively to the 90% allocation to cash at the target date of the Safe Landing Glide Path, saying things like “There’s no way that I’ll put my clients 90% in cash.” and “My clients won’t pay me to have 90% in cash.” These comments miss the fact that cash is excellent risk control, and controlling risk in the Risk Zone is what it’s all about. Dr. William F. Sharpe won the Nobel Prize in 1990 for the Capital Market Line shown in the following graph.

Dr. Sharpe showed that blending a broadly diversified world portfolio with cash dominates the efficient frontier at low levels of risk. You get higher returns with cash and the world than with portfolios weighted heavily in bonds.

With interest rates currently near zero, the theory is on even more solid ground because the risk in long-term bonds is high and the rewards are low.

Protect Yourself with Inexpensive Retirement Investing

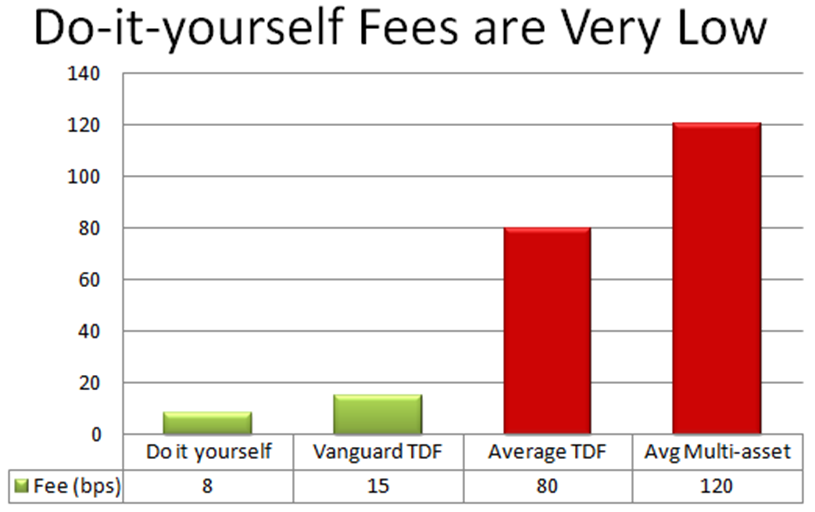

No one needs to settle for existing investment funds. TDFs and multi-asset funds are very expensive. All you need is a good glide path, like the Safe Landing Glide Path, and inexpensive exchange-traded funds (ETFs). If you use the lowest cost ETFs, you can create and track funds along your favorite glide path for less than .08% (8 basis point), far cheaper than the average mutual fund TDF and about half of the least expensive TDF mutual fund.

Here are the lowest fees currently available for the asset classes used in diversified TDFs:

| Asset Class | Lowest fee (basis points) |

| U.S. Stocks | 3 |

| Foreign Stocks | 6 |

| Real Estate | 7 |

| U.S. Bonds | 4 |

| Foreign Bonds | 19 |

| Short term Treasuries | 6 |

| TIPS | 5 |

We can help. We provide planning and investment services to guide adults through asset allocations for their lifetime. It’s a TDF customized to your needs and wants that is specifically engineered to protect you from a sequence of return risks, so you do better than off-the-shelf TDFs. You could go it alone, but we charge very little for the peace of mind that you are safe.

Conclusion

Despite their popularity, TDFs and IRAs are ticking time bombs that will destroy lifestyles when the next market correction occurs. This is a shame because the Safe Landing Glide Path can and should be the norm. Investors should be protected against a sequence of return risks.

Most Robo advisors serve millennials, but adults need the most help because retirement lifestyles are in great jeopardy and urgently need protection.

You can gain the double advantage of avoiding a sequence of return risks and paying very low fees. We can help. We provide all you need to manage your own Safe Landing Glide Path portfolio. Simply answer two questions:

- When do you plan to retire? Alternatively, when did you retire?

- What is your risk preference: conservative, moderate, or aggressive?

Voila, you get all the details you need to invest, and you can choose to modify as you’d like. Asset allocation is the ruler of investment performance and fees are its scepter.

In his Stock Market Counterfactuals, consultant Ben Carson observes:

The time to think about risk is when there is none. Think about how you can survive a downturn when stocks are rising and you feel good about yourself, not when they’re falling and it feels like the world as we know it is coming to an end.

Your current profits can be vaporized at any moment. If you underestimated your threshold for pain before volatility reappeared in 2018, now is a perfect time to reassess.

Please take our course on the Next 401(k) Scandal here https://learnformula.com/course/the-next-401-k-scandal-excessive-risk-in-target-date-funds

Ronald Surz is author of the book Baby Boomer Investing in the Perilous Decade of the 2020s .

Never miss a post.

We'll keep you in the loop with everything good going on in the modern professional development world.